Subject-To Real Estate: 10-Step Guide, Checklist, & Contract PDFs

Mar 28, 2025

Subject to real estate is undoubtedly one of the most strategic approaches you can explore when investing in real estate. If you're unfamiliar with the term “subject to mortgage” or the broader concept of “subject to” in real estate, you're in the right place.

In real estate investing, buying properties subject to the existing mortgage (often called “sub to contract”) is a creative financing strategy that allows investors to acquire property without having to qualify for a loan themselves. If you've ever wondered, “What is subject to in real estate?”, this guide will walk you through everything you need to know.

This guide aims to equip you with the necessary understanding, and for your convenience, we've included a subject-to-real-estate step-by-step guide, examples, sub-to-real estate contracts, and a comprehensive checklist.

- What Is Subject To Real Estate?

- How Subject To Works In Real Estate

- 3 Types Of Subject To Real Estate

- How to Find Subject To Properties For Sale

- How To Do A Subject To Transaction In 10 Steps

- Downloadable Subject To Real Estate Contract PDF

- Downloadable Subject To Real Estate Checklist

- FAQ: Subject To Real Estate

- Final Thoughts On Subject To Real Estate

Ready to Take the Next Step in Real Estate Investing? Join our FREE live webinar and discover the proven strategies to build lasting wealth through real estate.

Whether you're just getting started or ready to scale, we'll show you how to take action today. Don't miss this opportunity to learn the insider tips and tools that have helped thousands of investors succeed! Seats are limited—Reserve Your Spot Now!

What Is Subject To Real Estate?

"Subject to" real estate refers to the transaction of a property while maintaining the integrity of the existing loan on the parcel. If you're looking to understand how to buy a house subject to, this approach allows the investor to acquire the property without having to secure a new loan.

In subject to real estate, the investor purchases the property and agrees to make payments on the existing loan of the house. The seller gives the title to the real estate investor.

This loan stays in the seller's name, but the buyer makes the mortgage payments on behalf of the seller, and the lender does not know about the property's transaction.

How Subject To Works In Real Estate

When you engage in a "subject-to" real estate transaction, you essentially purchase the property while leaving the current mortgage intact.

This arrangement means that, as the investor, you shoulder the responsibility of the mortgage payments, even though the loan remains formally under the seller's name. The seller transfers the property title to you, but interestingly, the lender remains unaware of this transition.

This can be compared to a relay race where you, the new runner (or buyer), take the baton (property) from the previous runner (seller), continuing the race (mortgage payments). The original runner remains the officially registered participant, but you're now driving the pace and direction.

The seller benefits twofold: Firstly, they find reprieve from their mortgage obligations, which can be particularly beneficial in scenarios of looming foreclosures or financial duress. Secondly, they receive any agreed-upon difference between the property's market value and the outstanding mortgage amount.

From the buyer's perspective, this strategy can offer properties at attractive prices, potentially below market value, and often with established favorable loan terms.

However, it's important to note that the buyer needs to consistently honor the mortgage payments to prevent foreclosure since the property title is now in their possession.

For example, imagine traditional property sales as clearing off the entire mortgage at once and "mortgage assumption" as formally transferring the mortgage responsibility.

The "subject-to" strategy, on the other hand, operates in a grey area between these extremes. While there's typically no binding agreement detailing this setup, the repercussions of non-payment can be dire for the buyer, emphasizing the inherent responsibility this strategy demands.

Read Also: What Is An Assignment Of Contract In Real Estate?

3 Types Of Subject To Real Estate

Different “subject-to" strategies offer a particular niche that can be beneficial when understood deeply. There are primarily three kinds of "subject-to" real estate transactions:

-

Cash To Loan Subject To

-

Seller Carryback Subject To

-

Wrap Around Subject To

Let’s dissect each one to better comprehend their dynamics.

Cash To Loan Subject To

The most prevalent type of "subject-to" transaction, a Cash To Loan Subject-To, involves the investor paying the seller in cash for the difference between the property's current value and the outstanding mortgage balance. The investor then assumes responsibility for the remaining mortgage payments. In many situations, properties under this transaction type are nearing or already in foreclosure.

Cash To Loan Subject-To Example:

-

Imagine Mrs. Rodriguez wants to sell her house, which is valued at $350,000, but she still owes $310,000 on her mortgage.

-

Mr. Bennett, an investor, steps in and pays Mrs. Rodriguez $40,000 in cash, thereby covering the difference.

-

Mr. Bennett then continues to make payments on the original $310,000 mortgage.

Seller Carryback Subject To

A seller carryback subject to is the second most common form of a subject to. You're likely to have already heard of this type, just in different terms. This type of transaction is often called "owner financing" or "seller financing."

This works as an additional form of financing to be used if the investor's lender won't allow them the total funding that is needed for the purchase of the property.

The investor will get a mortgage for as much of the property's value as possible and then make payments to the lender in the form of a traditional mortgage, as well as payments to the seller in the form of a seller carryback, subject to.

The seller never gives the investor the difference in cash. Rather, they are not paid in full for their house and instead slowly receive the difference in payments directly from the investor.

The seller is in control of the terms of this transaction. They generally control the interest rate, downpayment, and loan length. Usually, the original homeowner wants the investor to put down a downpayment of five to twenty-five percent and pay off this portion in five years or less.

The official mortgage with the lender can take much longer to pay off and will likely be on different terms with different stipulations, down payments, etc.

Seller Carryback Subject To Example:

-

Mr. Anderson is selling his apartment for $400,000.

-

Miss Kim, the buyer, can only secure a loan of $350,000 from her bank.

-

To cover the remaining $50,000, Miss Kim and Mr. Anderson agree to a seller carryback arrangement.

-

She promises to repay him the $50,000 over 4 years at an agreed interest rate.

Wrap Around Subject To

The most intricate of the three, the wrap-around transaction, sees the buyer paying an interest rate derived from the original mortgage's rate but with an added premium. This ensures the seller can meet their own interest commitments to their original lender. This type can be more challenging for the buyer if the base interest rates are high.

If the original homeowner's mortgage is 4%, the seller will likely ask the investor to pay 6% on the carryback. At low interest rates, this isn't much of an issue. If, however, the seller had a higher interest rate, then this is not an ideal situation for the investor.

Wrap Around Subject To Example:

-

Mrs. Thompson is selling her vacation home with an existing mortgage that has an interest rate of 5%.

-

Mr. Wallace, an investor, agrees to a wrap-around subject-to deal where he pays an interest of 7%.

-

The additional 2% ensures Mrs. Thompson covers her interest obligations and gets a bit extra on top.

Read Also: Flipping Real Estate Contracts: A 6-Step Guide For Investors

How to Find Subject To Properties For Sale

Finding properties suitable for subject-to-transactions isn't all that different from sourcing regular real estate deals. The challenge is pinpointing homeowners willing to consider this non-traditional transaction.

Below are some tried-and-true methods to discover Subject-To opportunities:

Utilize Online Platforms

In today's digital age, several online platforms can aid you in identifying potential Subject-To properties. These websites are treasure troves for real estate enthusiasts, showcasing a plethora of listings, including those in distress.

-

The Multiple Listing Service (MLS): The MLS is a comprehensive source for real estate listings. Though mainly used by Realtors, it's an indispensable tool for dedicated investors.

-

PropStream: Offers detailed property data, including information about distressed properties and motivated sellers.

-

Foreclosure: As the name suggests, this site zeroes in on foreclosed properties, which are often ripe for Subject-To deals.

-

Zillow & Redfin: Both platforms have a pre-foreclosure filter that narrows down properties where homeowners might be facing financial strain and could be open to Subject-To agreements.

-

Mashvisor & RedX: These platforms provide data-driven insights on potential real estate investments, helping pinpoint viable Subject-To opportunities.

Harness Your Network

Real estate agents can be a treasure trove of information. Some have networks specifically catered to distressed properties or can point you in the right direction.

Real estate wholesalers typically have access to pre-foreclosure listings and can connect you with homeowners eager to sell.

Local real estate lawyers and attorneys often have knowledge about properties in pre-foreclosure or going through legal proceedings. Establishing a relationship with them can open doors to potential Subject-To deals.

Local newspapers are mandated to publish addresses of properties under foreclosure. This might sound old-fashioned, but it's a time-tested strategy to identify properties in distress.

Direct Mail & Driving For Dollars

Consider implementing a targeted real estate direct mail strategy. Craft well-thought-out letters or postcards expressing your interest in buying properties via Subject-To deals.

Zero in on neighborhoods or properties that appear distressed or vacant.

Driving for dollars involves driving around neighborhoods and scouting for properties that appear vacant or distressed. In doing so, you can find unexpected opportunities.

Engaging directly with homeowners gives you the chance to explain the potential benefits of a Subject-To deal, especially if they're in financial trouble.

Read Also: Real Estate Marketing Ideas: The 10 Best Campaign Strategies

Subject To Real Estate Pros & Cons

Subject-to real estate provides an array of benefits, easing the process for both investors and sellers but not without carrying some risks. Here's a deep dive into Subject-To’s benefits and drawbacks:

Benefits For Buyers & Investors

-

Easier Access to Property Ownership: Subject-to transactions pave the way for investors who might have inadequate credit or can't traditionally qualify for financing. This mode allows for the acquisition of property without the typical constraints of credit checks or financial backgrounds. For example, a young investor with a limited credit history can procure a property through a Subject-To agreement, bypassing the rigorous checks and requirements of conventional financing.

-

Cost Efficiency: Subject-To deals often exclude many intermediaries like banks, title companies, agents, or loan officers. This leads to reduced up-front costs, eliminating hefty closing costs, origination fees, and other associated charges. For example, a buyer interested in a house might find the closing costs too exorbitant to manage. Through a Subject-To transaction, they can purchase the same house while avoiding those additional expenses.

-

Accelerated Equity & Income Potential: With some part of the mortgage already settled, investors gain property equity swiftly. Moreover, Subject-To transactions, without the typical red tape, close faster than traditional realty deals, ideal for house flipping or quick turnover. For example, an investor eyeing quick returns might find a property with half its mortgage cleared. Procuring it via Subject-To lets them benefit from the existing equity, ensuring faster ROI when flipped.

Benefits for Sellers & Homeowners

-

Rapid Sales: For homeowners looking to swiftly transition to another property or needing a hasty sale for other reasons, Subject-To offers a quicker exit strategy compared to traditional methods. For example, a homeowner needing to relocate for a job can speedily dispose of their current property through a Subject-To deal, ensuring they move without the weight of the unsold house.

-

Financial Lifesaver: Homeowners grappling with foreclosures or urgent cash needs find a lifeline in Subject-To transactions. They can avoid foreclosure, safeguard their credit score, and sometimes even obtain instant cash. For example, a couple facing potential foreclosure can transition their mortgage to an investor using a Subject-To agreement, saving their credit score and avoiding the foreclosure mark on their record.

-

Bypass Repairs & Associated Costs: Many Subject-To deals accept properties in their existing condition, eliminating the need for repairs. This is a boon for sellers unwilling or unable to invest further in their property. For example, a property requiring substantial repairs can deter traditional buyers. However, a real estate investor might embrace the property 'as-is' in a Subject-To transaction, relieving the seller from repair hassles and expenses.

Risks For Buyers & Investors

-

Dependence On Seller's Honesty: When you venture into a Subject-To deal, you place trust in the seller to make regular payments to their lender using the funds you provide. However, if the seller defaults on their obligation, even if you've held up your end, the property might face foreclosure. For example, an investor diligently makes payments to a seller for a Subject-To property. However, the seller misappropriates the funds instead of settling the mortgage, leading to foreclosure, with the investor bearing the loss.

-

Potential for High-Interest Rates: In cases where the original property owner secured their mortgage with a less-than-stellar credit score, the inherited interest rate might be considerably high. Investors must be wary and evaluate the feasibility of such deals. For example, an investor takes over a property Subject-To, only to find out that the interest rate is significantly higher than market rates due to the original homeowner's poor credit history.

-

Insurance Challenges: Properties acquired through Subject-To agreements might face complications when trying to secure insurance. This can pose problems, especially for those intending to retain the property long-term. For example, an investor, after acquiring a property Subject-To, struggles to find an insurance provider willing to cover the property due to the unconventional purchase method.

-

Loan Acceleration Concerns: Certain Subject-To deals may have clauses allowing the lender to expedite the loan, demanding an earlier full payoff than anticipated. This can jeopardize the buyer's financial plans. For example, a buyer who anticipated years to settle the property's balance suddenly faces an immediate full payment demand due to a loan acceleration clause.

Risks for Sellers & Homeowners

-

Retention of Liability: Despite relinquishing the property and its equity to the buyer, sellers remain responsible for the original mortgage. If the buyer falters on payments, the seller might find themselves liable, and their credit score could suffer severe damage. For example, a seller enters into a Subject-To agreement, transferring their home to a buyer. Months later, the buyer defaults on payments. The mortgage provider, seeing the seller's name on the original loan, holds them accountable, damaging their credit score.

-

“Due on Sale” Clauses: Certain mortgages contain a “due on sale” provision that demands full payment of the remaining mortgage upon property sale. Even if not always enforced, lenders can invoke this clause, stripping sellers of potential profits from the sale. For example, a homeowner sells their property Subject-To, expecting to earn interest over time from the buyer's payments. However, their lender enforces the “due on sale” clause, requiring immediate settlement of the outstanding mortgage, depriving the seller of anticipated profits.

-

Reliance on Buyer's Commitment: Much like the buyer's dependence on the seller's integrity, sellers also place their trust in buyers to uphold their payment commitments. If a buyer defaults, sellers may need to undertake legal proceedings to reclaim their property, incurring further expenses. For example, a seller transfers their property to a buyer under a Subject-To deal. After a few consistent payments, the buyer discontinues them. Now, the seller has to navigate the legal system to retrieve their property and protect their financial interests.

Read Also: How To Invest In Real Estate: 10 Best Ways To Start Building Wealth

How To Do A Subject To Transaction In 10 Steps

The subject-to transaction allows buyers to purchase property without getting a new loan. This strategy requires meticulous attention to detail. Whether you're a seasoned investor or a newcomer, understanding how to execute a Subject-To deal can be a profitable venture.

Let's deep dive into our 10-step guide that will cover the process and set you on the path to mastering subject-to transactions:

- Find A Distressed Property Owner

- Engage With The Homeowner & Collect Relevant Data

- Analyze Your Potential Investment

- Visit The Property

- Do Your Due Diligence

- Calculate Your Expected Expenses

- Make An Offer To The Homeowner

- Organize & Ready Your Purchase Documents

- Close On The Property & Get Your Keys

- Take Care Of The Insurance

1. Find A Distressed Property Owner

Finding a distressed property owner is the foundational step in a subject-to transaction. These homeowners are typically facing financial hardships, making them more inclined to consider unconventional selling methods.

For your reference, here are the resources we mentioned above to kick-start your search:

-

Mashvisor.com: A platform dedicated to real estate analytics, Mashvisor can offer insights into potential distressed properties and markets.

-

Zillow.com: By filtering results to display only pre-foreclosures, this popular real estate marketplace becomes a goldmine for potential subject-to deals.

-

Foreclosure.com: As the name suggests, this site is dedicated to listing properties that are either in foreclosure or at risk of foreclosure. Don't forget to check out our review for a comprehensive understanding of the platform.

-

RedX.com: Another platform to consider, RedX specializes in offering lead solutions, which can be instrumental in finding distressed property owners.

-

Your local newspaper: Often overlooked in the digital age, local newspapers remain a traditional method to find distressed properties. They are mandated to publish addresses of properties undergoing the foreclosure process.

-

Real Estate Wholesalers: These are individuals or entities that subject to contracts with a seller, then sell the contract to an end buyer. They often have access to off-market deals and distressed properties.

-

Real Estate Attorneys: Leveraging the connections of local attorneys can be invaluable. They're often privy to information about homeowners facing legal challenges related to their properties.

-

Driving for Dollars: A grassroots approach, this method involves driving around neighborhoods, looking for signs of distressed or vacant properties, and then reaching out to the homeowners directly. It's an active, ground-level strategy that requires dedication but can yield significant results.

2. Engage With The Homeowner & Collect Relevant Data

Approach the situation with empathy and professionalism. Remember, the homeowner might be going through a difficult phase, so always lead with kindness, understanding, and respect.

Identify the root cause of the homeowner's predicament to gauge their eagerness to sell.

Inquire about essential details such as the lending institution, outstanding loan amount, monthly mortgage payment, and any overdue payments. Additionally, gather information about potential tax liens and mechanic liens on the property.

Ensure the homeowner provides you with an "Authorization to Release Information" form. This isn't a tactic to question their integrity but is crucial to validate the data they've shared. By doing so, you can guarantee that you present them with the most equitable and optimal offer for their residence.

3. Analyze Your Potential Investment

Begin by determining the after-repair-value (ARV) of the property. Estimate the rehabilitation expenses and chalk out your prospective exit plan.

Evaluate the prospective property in relation to its neighbors, considering its current state and potential post-renovation.

Conduct a comprehensive sales comparison analysis, ensuring you adjust for differences in property attributes such as amenities, square footage, and the number of rooms, specifically bedrooms and bathrooms.

Define your endgame. Are you looking to resell the property at a profit, convert it into a rental unit, or explore a lease option? For a resell, benchmark against recent sales in the vicinity. If considering it for rental, assess local rental rates. And if opting for a lease, compare terms with nearby lease agreements.

4. Visit The Property

Get permission from the homeowners and then visit the house. This will fill in the blanks on repairs you'll need to make, the condition of the property, and how long it will take you to fully rehab the home. Take pictures if you've been given permission, and don't forget to bring your checklist. We'll provide you with that checklist down below.

If you can get a home inspector to tag along with you, that's even better.

After your visit through the property, you may need to revisit step three and adjust your estimates.

5. Do Your Due Diligence

The experienced investor knows to never, ever skip this step. This isn't exactly a fun part of real estate deals, but it is crucial to protect yourself and ensure a smooth, profitable sale.

If you haven't already, get the seller to sign an "Authorization to Release Information" form. Once this form is signed, call their lender and fax or email this form to them. After they see you have the authorization, the lender will give you lots of really important information regarding your potential new property.

Next, have a title company run a preliminary title search. This will tell you who the complete list of owners are, and if there are any liens or owed taxes on the property. During this search, you may find that tax liens, mechanics liens, HOA liens, code enforcement liens, or Federal IRS liens are owed against the property.

Then, you should also call all of the local utility companies to get information on the property. Utility companies you should be checking with to see if there are any past-due bills include:

-

Water Company

-

Electric Company

-

Sewer Company

-

Trash Company

-

Internet, Cable, Landline Company

-

Alarm System Company

After checking on the utilities, check the property tax amount. This will let you know when and what to expect to pay in property taxes once the parcel is yours. It will also let you know if the current homeowner is behind on any of these taxes and how much money will be owed once you make the purchase.

6. Calculate Your Expected Expenses

Anticipate various expenses associated with acquiring the property to ensure a smooth transition. Potential costs you may incur include:

-

Seller for their accrued equity, which may equate to the portion of the loan they've settled

-

Outstanding mortgage payments to bring the account current

-

Closing costs such as transfer charges, governmental levies, escrow expenses, legal services, and title insurance protection

7. Make An Offer To The Homeowner

Using all of the above information that you've gathered, make a fair offer to the homeowner for their property.

-

You may offer to take over payments for the homeowner without paying them any cash.

-

You may offer to take over payments for the homeowner and pay them some lump sum of cash to cover their equity in the property. Usually, this is because they owe less than what the property is worth.

-

You may offer to take over payments for the homeowner and negotiate that they pay you to take this property off their hands. Usually, this is because the owners owe a lot more money on the mortgage than what the property is worth.

It's always a good idea to have a real estate mentor or real estate attorney help you draft an offer. They can accurately tell homebuyers if the existing loan balance is appropriate and what a fair purchase price should be.

8. Organize & Ready Your Purchase Documents

For this step, you need a purchase document that is enforceable in your state. At the bare minimum, have your subject-to-agreement checked by a real estate attorney. Better yet, have your attorney write up the subject to document for you.

Your real estate attorney is already knowledgeable about loan terms, a fair sales price, and how to make a proper loan assumption. They are good people to have on your team.

9. Close On The Property & Get Your Keys

Depending on the state, you can finalize the property transaction at home with the seller, at a title company, or with a closing attorney.

While "kitchen table" closings are valid in some states, they are almost never a good idea. It's wise to stick to attorneys and title companies for the most financial safety.

Most closing documents will need to be notarized, which is why kitchen table sales are such a bad idea. All owners will need to present to sign the documents, and that includes spouses. If an owner has died, a death certificate will likely be needed to make the transaction.

At closing, you will receive your new investment property's keys.

10. Take Care Of The Insurance

First, you will need to cancel the seller's insurance. Use your limited power of attorney to change the mailing address to your address, and then cancel their homeowner's insurance policy.

Next, you'll need to obtain your own homeowner's insurance. You should always have your own policy on the house to ensure that you are never denied a claim. This can happen if the primary insured person is not the owner.

When you create your new policy, make sure that you get a non-owner-occupied landlord policy. You need to be the first name listed on the insurance, and then the existing mortgage company as the mortgagee. Make the seller the additional insured on the policy.

Read Also: Wholesale Contracts In Real Estate: FREE PDF & Template

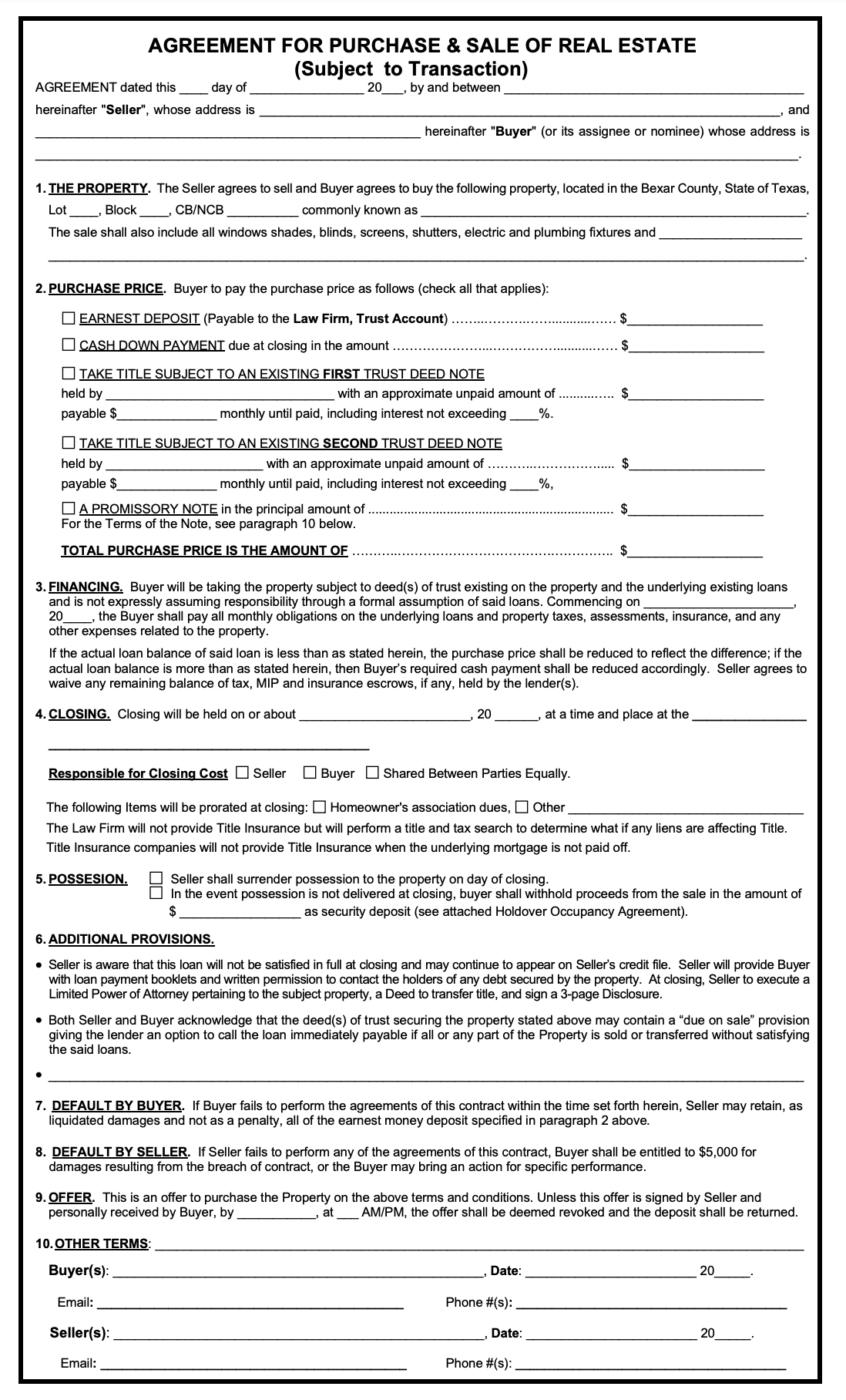

Subject To Real Estate Contract PDF

You should contact your real estate attorney for a sub to contract PDF or an agreement for the purchase and sale of real estate subject to transaction.

With that said, here is an example of a simple subject to agreement. Use this just to get an idea of what to expect:

Subject To Real Estate Checklist

For a comprehesive, step-by-step document, here is a downloadable subject to real estate checklist PDF. Again, speak to your mentor, or better yet, a subject to real estate attorney, for complete safety and coverage. Use a home inspector during step four if at all possible.

FAQ: Subject To Real Estate

“Subject to” is one of the most misunderstood but powerful strategies in real estate investing. If you’re new to creative financing, this section will help you quickly grasp the essentials. Below are common questions about subject to real estate and how this method can help you build a portfolio with less cash upfront.

What does subject to mean in real estate?

In subject to real estate, an investor buys a property while leaving the seller’s existing mortgage in place. The investor takes control of the property but does not formally assume the loan.

Is subject to real estate investing legal?

Yes, subject to real estate deals are legal in most states when done correctly with full disclosure. It’s important to consult an attorney and follow state-specific laws.

Why would a seller agree to a subject to deal?

Sellers may agree to a subject to real estate transaction if they’re behind on payments, facing foreclosure, or need to get rid of a burdensome property quickly. It can help them avoid damage to their credit and offload a financial burden.

Do I need good credit for a subject to real estate deal?

No, you typically don’t need good credit or to qualify for a new loan in a subject to real estate deal. That’s part of what makes it attractive to newer investors.

Who pays the mortgage in a subject to deal?

The investor takes over responsibility for making the monthly mortgage payments in a subject to real estate transaction. The loan remains in the seller’s name, but the investor pays it.

Can I resell or rent a subject to property?

Yes, once you acquire the property through a subject to real estate deal, you can rent it out, sell it, or even rehab and flip it. You have full control as the new owner.

What are the risks of subject to real estate investing?

The biggest risk in subject to real estate is the lender calling the loan due through the due-on-sale clause. Proper structuring and working with professionals can minimize this risk.

Final Thoughts On Subject To Real Estate

Subject to real estate might appear daunting initially, but with the right knowledge and approach, it's entirely manageable. Both the seller and the investor stand to gain from such transactions.

Sellers can sidestep potential financial setbacks, foreclosures, or severe credit impacts while also potentially securing an expedited sale, sometimes even with immediate cash returns.

On the flip side, for investors, the allure of subject to real estate lies in its convenience: no need for rigorous credit evaluations, minimal or zero down payments, and a swift closing process.

Ready to Take the Next Step in Real Estate Investing? Join our FREE live webinar and discover the proven strategies to build lasting wealth through real estate.

Whether you're just getting started or ready to scale, we'll show you how to take action today. Don't miss this opportunity to learn the insider tips and tools that have helped thousands of investors succeed! Seats are limited—Reserve Your Spot Now!

*Disclosure: Real Estate Skills is not a law firm, and the information contained here does not constitute legal advice. You should consult with an attorney before making any legal conclusions. The information presented here is educational in nature. All investments involve risks, and the past performance of an investment, industry, sector, and/or market does not guarantee future returns or results. Investors are responsible for any investment decision they make. Such decisions should be based on an evaluation of their financial situation, investment objectives, risk tolerance, and liquidity needs.

Alex Martinez, the founder of Real Estate Skills, is known for his strong, practical expertise in real estate, starting from a beginner with no family connections in the industry to completing over 50 real estate deals, including wholesale and flips, within his first year.

He has dedicated his career to providing cutting-edge education and resources for real estate professionals. He emphasizes the importance of self-taught knowledge through mentors, books, and hands-on experience.

His journey from earning a modest income to becoming a successful real estate entrepreneur and educator showcases his expertise and dedication to the field.

Ryan Zomorodi, co-founder and COO of Real Estate Skills, leverages his experience from a diverse background in real estate investment, construction management, and entrepreneurship to provide comprehensive education in the real estate sector.

His expertise is rooted in hands-on experience, extensive industry knowledge, and a commitment to empowering others through education.

Ryan's journey reflects a blend of practical experience and entrepreneurial success, contributing to his role in developing a platform that educates and supports aspiring real estate professionals.

Read Ryan's Full Bio >>

Access Our Brand-New Free Training

Learn how to consistently find real estate deals for wholesaling & house flipping.

We recommend Colibri Real Estate School for getting licensed. Click the button below to get started!